Credit Cards with Annual Fees: Are They Worth It?

When shopping for credit cards, you may be surprised at the steep annual fee for some of the premium cards out there. Those gold-star perks do come with a price: in some cases, several hundred dollars and upwards. So when is the annual fee worth it? We’ll walk you through some of the factors that you should consider if you’re shopping for credit cards.

Here’s what we’ll cover in this post:

When do you pay an annual fee on a credit card?

When are credit cards with annual fees worth It?

You want better cash-back rewards than what a free card offers

You can offset the fee with spending rewards

You have a bad or limited credit history

The full set of benefits work for you

More tips for credit card annual fees

Track the perks you’ve cashed in on

Remember to review annually

It’s okay to contact the credit card company to negotiate

Consider comparable cards

Credit card annual fees: key takeaways

Click one of the links above to jump straight to a section, or read through for a more thorough look. We’ll start by answering a simple question: what are annual fees, anyway?

What are annual fees?

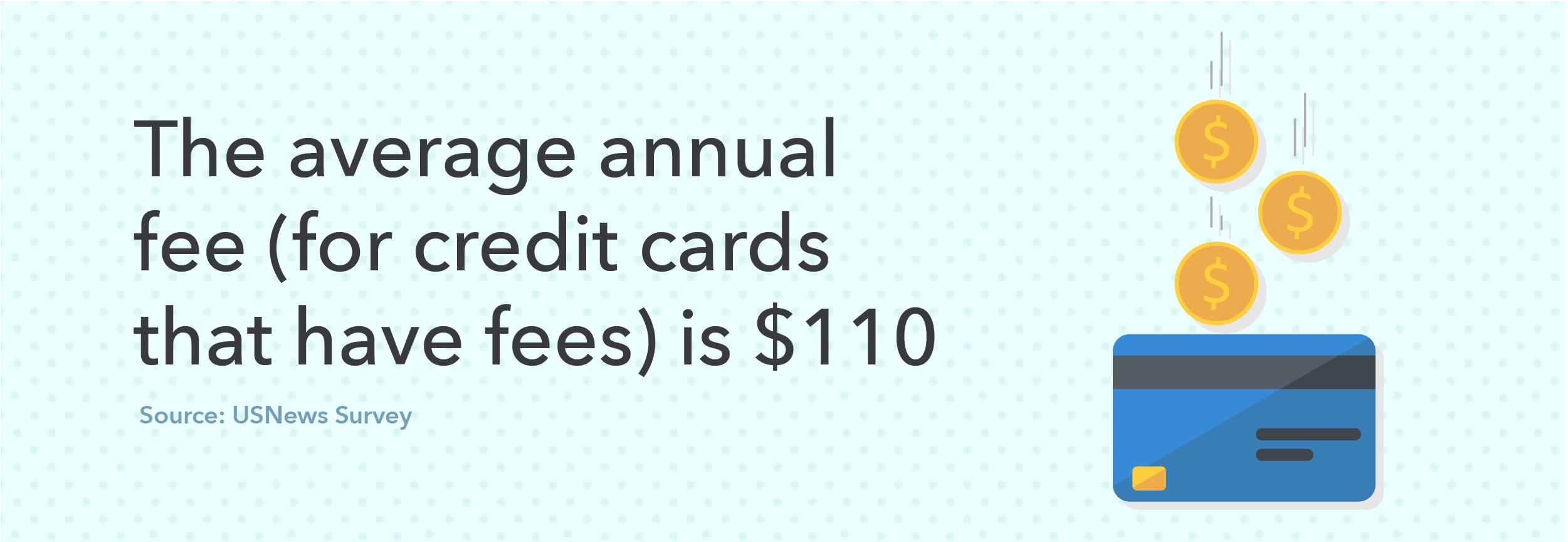

Annual fees are pretty much what they sound like: they’re a price that you pay each year in order to keep your credit card open. According to a USNews survey, around 70% of credit cards do not charge an annual fee. Of the cards that do charge an annual fee, the average amount was $110. However, there are plenty of other options, as this Credit Karma list shows, for under that price.

When do you pay an annual fee on a credit card?

Generally, annual fees are charged just once a year in the same month each year. Credit card companies often use the month you opened your credit card as the month they charge you your annual fee. So, if you opened a new card with an annual fee in March, you’ll likely be charged that fee again the next March.

When are credit cards with annual fees worth it?

There are a few different ways that you can assess whether a credit card with an annual fee is worth it. To find out more, we spoke with personal finance experts to uncover what they look for in a credit card with an annual fee.

You want better cash-back rewards than what a free card offers

Simply put, you’ll want to make sure the perks outweigh the costs. So, if that travel rewards credit card charges a $100 annual fee, if you get over $200 in miles or points toward free travel, paying extra for that card might be worth it.

What to look for includes higher than average reward points per dollar, plus the extra features and travel-related benefits. With cashback cards, it’s easy to calculate the break-even point, explains Eric Rosenberg of Personal Profitability. “You can do a little math to figure out exactly what you need to spend on the card annually to earn back your fee and make a profit.”

You can offset the fee with spending rewards

Another way to gauge whether a premium credit card is worth the annual fee is to assess three major things: 1. short-term value, 2. day-to-day value, and 3. experiential value through travel benefits, says Kathy Hart, a travel hacking enthusiast.

Short-term value is the generous introductory bonus that comes with many premium credit cards. For instance, on some cards, you can earn 50,000 bonus points if you spend $3,000 on your card within the first three months.

Day-to-day value is how many points you’ll net for everyday purchases. Some offers include up to three points for every dollar in certain categories. You can also score more points for rotating spending categories, such as groceries in the fall, or gas during the winter months.

Experiential value means all the neat travel and other perks that are widely promoted. This could include some sweet perks such as free rideshare while travelling, meals on flights, and access to airport lounges replete with yummy snacks and beverages. Some cards may offer several hundred dollars in travel or store credit that you can use each year.

A word of caution: It’s not smart to use credit cards unless paying the balance in full every month, points out Hart. “The benefits of travel points are negated if you are paying credit card interest or fees,” she says. If you’re just starting out, start slowly.

You have a bad or limited credit history

Credit card companies may sometimes use an annual fee as a way to make credit cards available to people with rougher or limited credit histories. If you have a poor credit score, it can be difficult to successfully apply for a card, as companies may be hesitant to lend to you. And, while there are annual-fee-free credit cards marketed toward people with low credit, many times credit cards for rougher or absent credit profiles do charge a fee.

What’s a good credit score? Read our blog post to find out more.

For some people, a card with an annual fee is the only or the best option. If that’s the case for you, then it may be wise to invest in the annual fee as a way to start building or repairing your credit.

The full set of benefits work for you

Besides the premium, heavily advertised perks of a credit card, you’ll want to get acquainted with your card’s full suite of benefits, says Lee Huffman, a personal finance and travel writer. “There are often underused perks—like price protection, VIP lounge access, purchase protections, extended warranty coverage, or primary rental car insurance—that can really provide huge value for you if you knew they were part of your card benefits.” You’ll want to compare these benefits with the other cards to see if you should keep it or apply for another one.

More tips for credit card annual fees

If you already have a credit card with an annual fee, it’s a good idea to keep tabs on it and ensure that it’s still worth it for you. Just because it was worth the cost last year doesn’t mean it will be this year or next. Here’s what you can keep in mind as you assess.

Track the perks you’ve cashed in on

Sure, there may be perks. But are you taking full advantage of them? Keep tabs on all the perks you’re raking in, estimate how much each perk is worth, then do the math to figure out if the fee is worth it. “Evaluate whether you are utilizing the benefits of the card,” says Hart. “ If you find you’re not using the card, see if you can downgrade it, or switch to a card that has a lower—or no annual fee.

Remember to review annually

To make sure the annual fee is worth it, review your cards annually. “Credit card benefits are constantly changing, so a card that worked perfectly for you last year, may not be the right one going forward,” says Huffman. “Make sure the bank is earning your business every year.” For instance, if one of your platinum cards starts to limit lounge access or reduces the number of free luggage, consider not renewing the card when the fee is due.

Another way to see if the card is worth its weight in annual fees? Add up all the value of the rewards and benefits the card offers you, but then to subtract what you would have received if you switched to the next best card with an annual fee, suggests Steele. If the difference is more than the cost of the annual fee, then the card’s a keeper.

And you’ll want to track your use as an individual that year, not just how much the card offers. So even if the card offers several hundred dollars in travel perks, but you only use, say $100 and the card has a $150 annual fee, it may not be worth it to you. And maybe the perks you end up using the most changes. And if the perks you end up using the most change you’ll want to take that into consideration.

It’s okay to contact the credit card company to negotiate

Flex your negotiation muscles and see if the credit card company is willing to issue a credit card annual fee waiver. The best time to do it is right before the annual fee is due points out, Huffman. Let the credit card issuer know you’re considering closing the card because you’re not sure if the benefits are worth the annual fee any longer.

You just might be able to get them to maximize credit card rewards to sweeten the deal. “It doesn’t work 100 percent of the time,” adds Steele, “but I’ve been successful enough that it’s worth the call.”

Before reaching out to the credit card issuer, do your homework. If you’re a customer with solid credit and have been stellar at making on-time payments, you’ll have more leverage. Plus, see what existing cards have comparable rewards and benefits with lower fees.

Consider comparable cards

Wondering if you should switch to another credit card? The trick is to add up the total value of a card’s rewards and benefits, then subtract what you would’ve received if you switched to the next best card with an annual fee, says Jason Steele. If it ends up not being worthwhile, it might be time to switch to another credit card.

While you may initially experience sticker shock with those platinum credit cards that come with a, say, $450 annual fee, if you would end up benefiting from the travel-related and rewards points, it could end up being worth that extra chunk of change.

Credit card annual fees: key takeaways

A lot to digest? Don’t worry — here’s what to remember:

Annual fees are fees that you pay once a year for the right to use a credit card. Usually, they’re charged in the same month you first opened the card.

While this may seem like a bad deal, there are some cases where an annual fee credit card can make a lot of sense:

The perks, like cash back and travel miles, add up to more than the annual fee cost

The perks fit in well with your lifestyle and are better than what a free card offers

You have limited or low credit, and an annual fee credit card is your only option

If you already have a card with an annual fee, remember to re-assess each year to determine whether it’s still worth it. You may even be able to negotiate better perks or a lower fee if you’ve used the card responsibly.

You can always consider better cards if you find that yours is no longer working for you.

Remember, no matter what credit card you choose to use, you can always link it up with the Mint app for a quick bird’s-eye view of how your card fits into your finances.

The post Credit Cards with Annual Fees: Are They Worth It? appeared first on MintLife Blog.